If you’ve been watching home prices and thinking, “Did my budget shrink overnight?” you’re not alone. Home values have continued to rise, and the Federal Housing Finance Agency (FHFA) reported about a 3.26% increase last year. Because loan limits are tied to home price trends, conforming loan limits increased too. This is particularly important for those considering a mortgage.

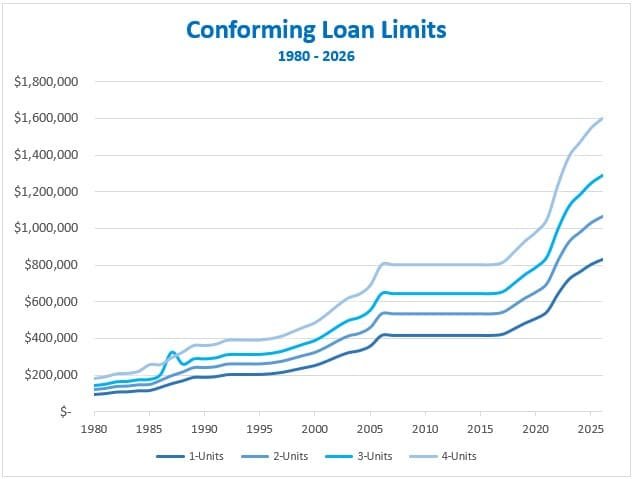

Starting January 1, 2026, the new conforming loan limit is $832,750 in most U.S. counties, up from $806,500 in 2025. In high cost areas, the limit increased to $1,249,125, up from $1,209,750.

This matters because conforming loans are often one of the most common, flexible, and widely available ways to finance a home mortgage.

What is a conforming loan limit

A loan limit is simply the maximum loan amount allowed for a certain loan category. It does not control the home price you can buy. It controls how the loan is classified.

In simple terms, loan limits help draw a line between two worlds.

Conforming loans, which follow Fannie Mae and Freddie Mac guidelines

Non conforming loans, which go above those limits and are often called jumbo loans

That line matters because the loan type you fall into can change how the loan is priced, how it is approved, and how strict the qualification rules may be.

Why conforming loan limits exist

Fannie Mae and Freddie Mac support the mortgage market by buying conforming loans from lenders. That helps keep mortgage lending stable and widely available.

Loan limits are part of how that system manages risk. Instead of allowing very large loans into the same system, limits keep the program focused on typical home buyers across the country.

As home prices rise, the limits usually rise too, so buyers are not pushed into jumbo loans just because the market got more expensive.

What a conforming loan is, in plain English

A conforming loan is a conventional mortgage that meets these rules.

It is not backed by the government, so it is not FHA, VA, or USDA

The loan amount is within the county loan limit

The borrower and the loan meet Fannie Mae and Freddie Mac guidelines

Because these loans fit a standard set of rules, they tend to be easier to compare across lenders. They also usually offer more consistent terms from one lender to the next.

Why this change matters for buyers

When conforming limits go up, it can help buyers in a few important ways.

More homes and price points may qualify for conforming financing

Some buyers may avoid jumbo loan requirements

Borrowers may have more flexibility with how they structure their down payment and loan amount

This can be especially helpful in markets where prices are close to the prior limit. Even a modest increase can keep more buyers in the conforming category.

County by county limits are a big deal

Not every county has the same limit. Some areas are considered high cost and have higher limits. FHFA publishes a county by county list and an interactive map.

This is important because two buyers purchasing similar homes can fall under different rules depending on where the property is located.

If you are buying in Arizona, the best move is to confirm the county limit using the property address instead of guessing.

What if your loan amount is above the limit

If the loan amount exceeds the conforming limit, it becomes non conforming. That does not mean you cannot buy the home. It just means you may be looking at jumbo financing or another structure.

Jumbo loans can be a great option, and rates are not always worse. The bigger difference is usually qualification.

Many jumbo programs require stronger credit

Some require more cash reserves

Debt to income limits may be tighter

Documentation may be reviewed more closely

The right answer depends on the full picture, not just the loan size.

The bottom line

The 2026 conforming loan limit increase is good news because it keeps lending options aligned with real world home prices. It gives many buyers more room to finance a home with a conventional conforming loan, especially in areas where prices have been pushing buyers into jumbo territory.

Next step

If you tell me the city or county where you’re looking and your rough price range, I can quickly confirm the county loan limit and show you the cleanest loan options for your situation.